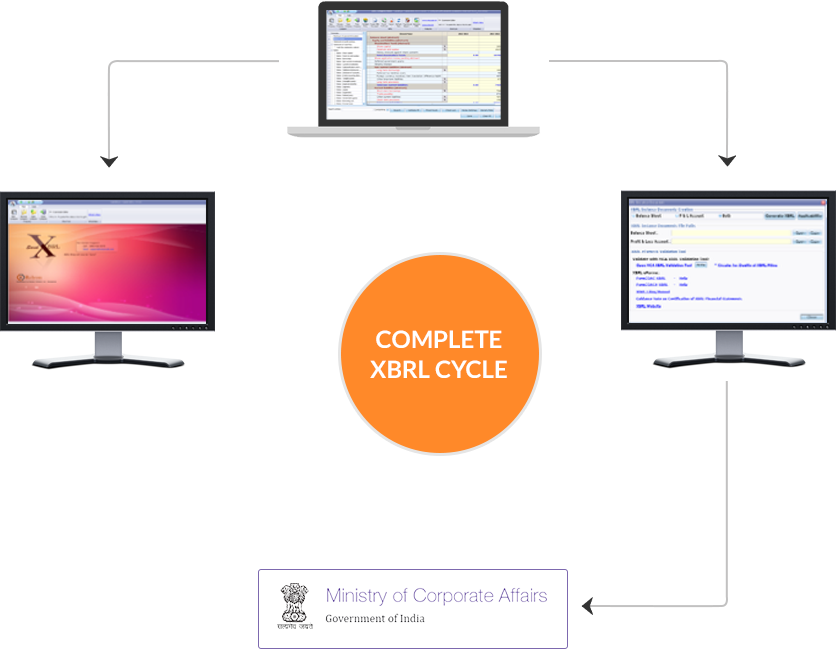

Complete XBRL Taxonomy flow

One stop Solution for return filing of XBRL with MCA as per the prescribed taxonomy, from Company details entry to submitting Form 23AC and Form 23ACA in single flow

One stop Solution for return filing of XBRL with MCA as per the prescribed taxonomy, from Company details entry to submitting Form 23AC and Form 23ACA in single flow

An easy Solution for return filing of Cost and Compliance Report for the required industry as per the taxonomy given by MCA

The Company information can be auto fetched from MCA server on providing the CIN of the company. Similarly, the directors information can be fetched on providing the DIN of the director

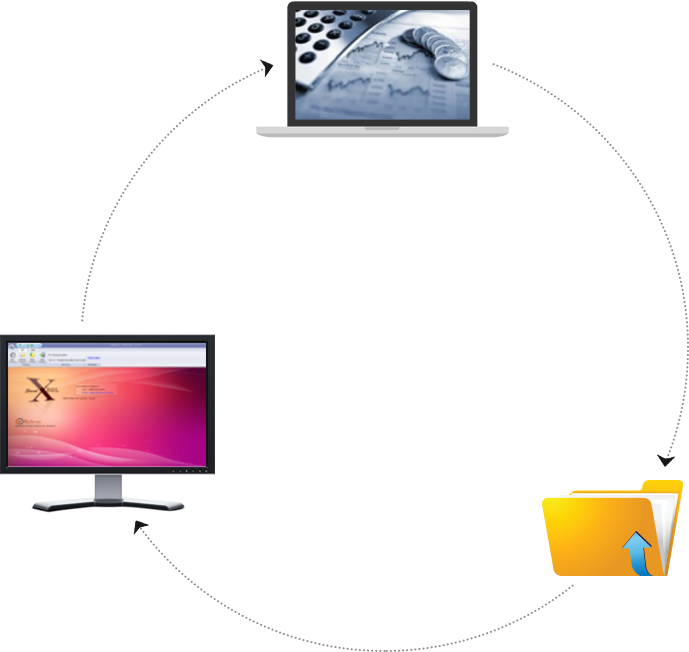

All the details of the Annual report, Financial and Non-Financial details, can be imported from the Word document or Excel file or PDF Document

The entire Business rules for filing XBRL with their relevant FAQs are pre-loaded in the software at the relevant screen to help the user to ease their work of data entry